At Giving What We Can we believe in not only in donating to the most effective, high impact charities in need of funding, but we also believe that when giving it is important to make prudent and informed tax-deductible donations to make your money count the most where it possibly can.

Before making a donation, there are some important rules you should be aware of that govern the gifting of money to charity.

Put simply, there are two facets to pay attention to when thinking about tax and giving:

- Is my chosen charity eligible for tax deductions/ Gift Aid?

- How can I reduce my own tax bill by donating?

Whilst there are no legal restrictions to the amount of charities you decide to support or the size of the donation you want to make to a registered charity, at Giving What We Can we advise against breaking a donation up between multiple charities when giving small amounts, as this reduces the impact your donation can have. There are some tax implications to consider before going ahead with your donation. It might seem like a lot of extra effort to go to, but by making tax-efficient donations you can substantially increase the value of your donation to your chosen charity. What’s more, by making charitable donations it is also possible to reduce your own income tax bill if you are in the higher earning bracket. Here are a couple of the most tax-efficient schemes to look out for:

For UK Taxpayers:

Gift Aid

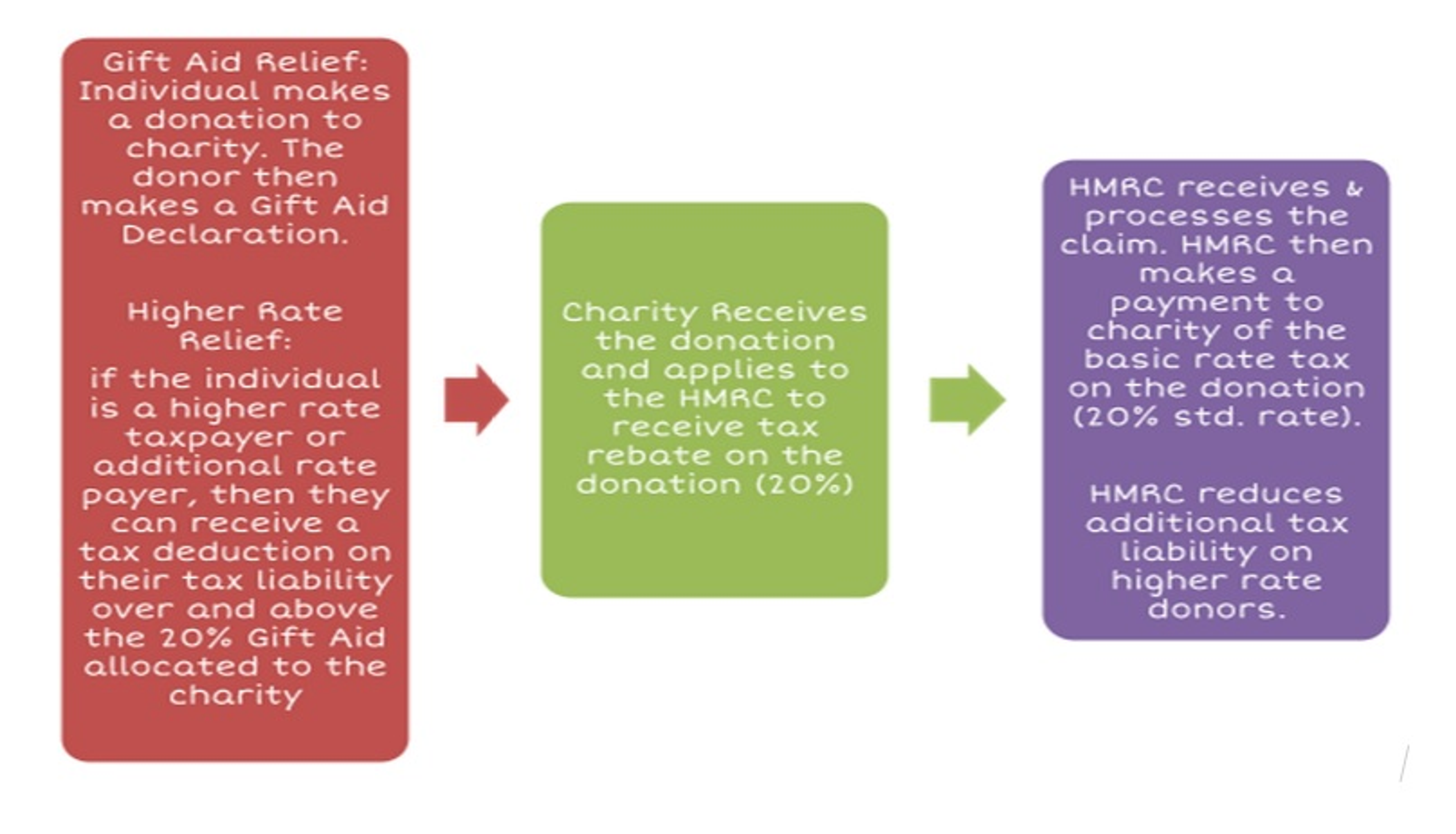

Gift Aid was a scheme introduced by the UK government to support registered charities. This scheme allows registered charities to reclaim income tax in order to boost the value of donations made. As income is so variable and for simplicity’s sake, charities can only reclaim income tax at the basic 20% rate on each donation. In practice, this means that if you donate £10, the charity will actually receive £12.50 by claiming back on Gift Aid, plus additional government subsidies that we won’t go into here.

Additionally, if you are a higher income taxpayer who pays a 40-50% tax rate (i.e. if your income falls in the region of £41,866 - £150,000+ per annum) , you are eligible to reclaim the difference of the 20-30% you were charged on top of the deductible 20% Gift Aid rate the charity receives.

In the 21 years since Gift Aid was introduced, registered charities have garnered an additional £12 billion in tax reclaims on donations in the UK. However, the Charities Aid Foundation (CAF) estimates that an additional £750 million pounds of potential tax reclaim benefit goes unclaimed each year. This represents a vast loss of resources that could be materially changing and saving lives if allocated effectively!

How Gift Aid Works:

In order to claim any tax benefits for both yourself and the charity, the organization you are donating to must be a registered charity for tax purposes by the HM Revenue and Customs (HMRC). You can check this by looking for the charity’s HMRC reference number on their website or by asking your charity to confirm that it has an HMRC charity reference number if you cannot find it listed online. Gift Aid can be applied to any UK, EU, Norwegian or Icelandic charity that is registered with the HMRC, but you have to be a UK taxpayer to be eligible for Gift Aid.

If your donations are made under the Gift Aid Scheme, you may need to fill out a Gift Aid Declaration Form in order for your charity to claim tax back on your donation. This form authorizes the charity to claim Gift Aid on your behalf. In order to be eligible for Gift Aid, you must be a UK taxpayer and have paid enough income tax or capital gains tax to cover the amount the charity will reclaim on your donation.

If you haven’t paid enough Income Tax this year to claim the 20% Gift Aid tax rebate on your donation, it is possible to "carry back" and reclaim Gift Aid on donations from the previous tax year by completing a request via a Self Assessment Form, or by contacting your local tax office.

You will need to keep records of all donations you make to registered charities including the dates and amounts, as well as any receipts for bank transfers or cash donations. Details about how to record your donations can be found here.

You can make a Gift Aid eligible donation to one of our recommended charities here.

Information for Higher Rate Taxpayers:

If you require tax reclaims as a higher rate taxpayer (paying tax at 40% or more), you will need to either fill in a Self Assessment tax return form to the HMRC or request that the HMRC amend your tax code.

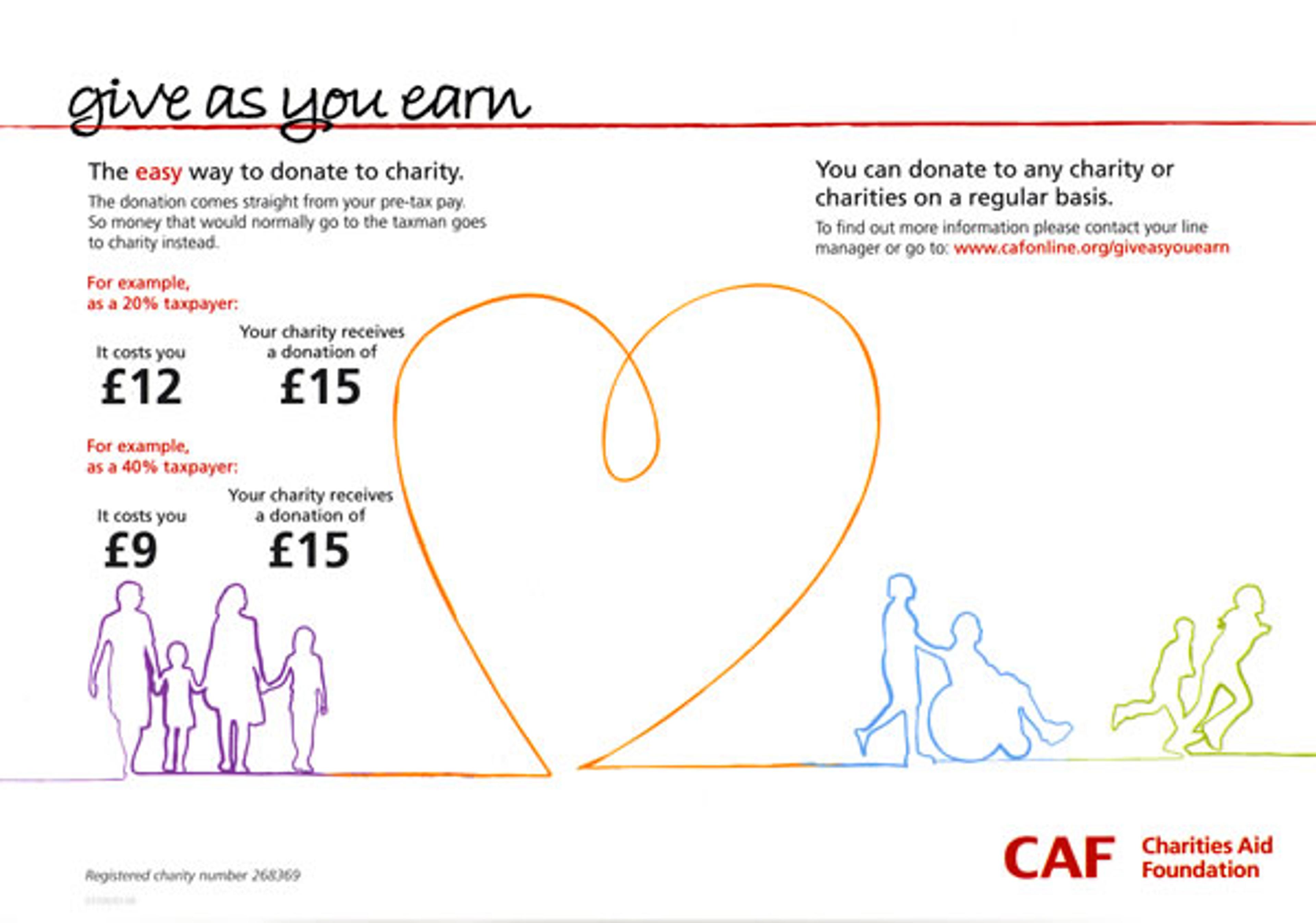

Giving through your pay or pension to charity

You can also give money to charity directly from your pay or personal pension by using the Payroll Giving scheme in the UK. This is an easy way to increase the value of your donation at the least cost to yourself, as your donation is deducted from your gross salary BEFORE tax, so you don’t pay any tax on it. For example, if you give £1 through PayRoll Giving, it will only cost you 80p before tax, and 60p if you are a higher rate taxpayer.

Using the Payroll scheme you can give to as many charities as you like and you can cancel your Payroll giving agreement at any time.

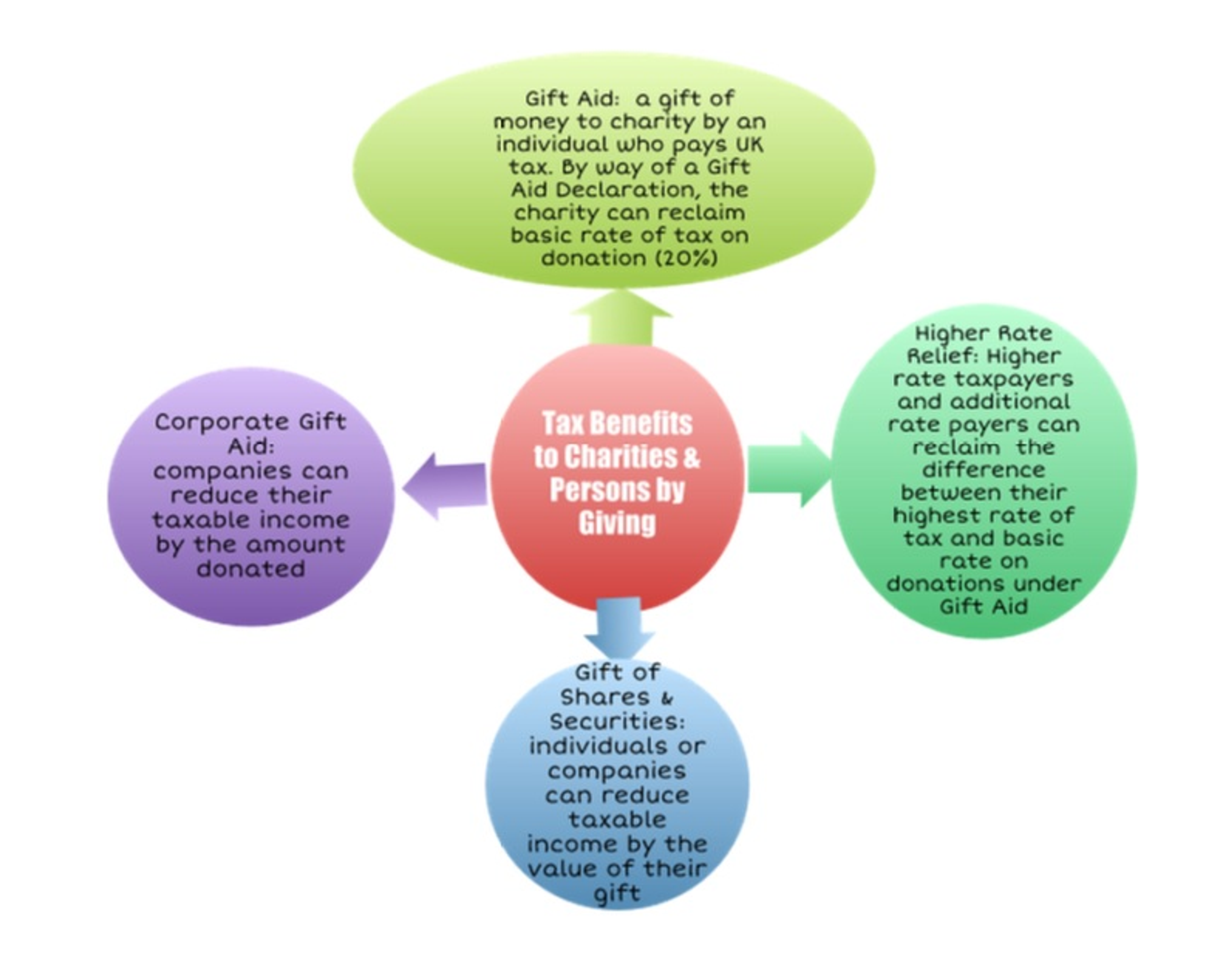

Capital Gains Tax

Capital Gains Tax refers to the tax that is due when you give away, sell, exchange or otherwise dispose of certain assets such as shares or property, and by doing so you exceed your annual exemption limit for that tax year. In the UK, this is currently £10,900 for each individual and £5,450 for most trustees in the current tax year of 2014. All gifts to charity qualify for Capital Gains Tax Relief. In practice, this means that all gifts to charity are exempt from tax. Additionally, in some cases you can file these donations as losses to reduce your Capital Gains Tax liability elsewhere.

Declarations of capital gains and losses are made through the Self Assessment tax return system; for more information on what you need to report, visit the HMRC website. Usually you don’t need to complete a self assessment tax return, but you will need to complete a Self Assessment registration form in order to declare Capital Gains.

Income Tax relief on Gifts of Shares/ Assets:

Income Tax refers to the tax on your income. Your income includes the earnings you make from employment, interest on savings or income from rentals or a trust and your pension.

You can claim Income Tax relief on gifts and lower your tax bill if you:

- Give land or buildings in the UK or qualifying shares to a charity;

- Sell these to a charity at less than their market value;

Qualifying shares include those listed on any stock exchange.

Income Tax relief works a little differently to Capital Gains Tax relief in that not all gifts to charity are eligible for Income Tax relief.

The assets on which you can claim Income Tax relief are restricted to the following:

- Shares and securities listed on the UK or another internationally recognised stock exchange;

- Units held in a FCA authorised unit trust;

- Shares held in a UK OEIC (Open Ended Investment Company);

- Certain foreign collective investments – similar to OEICs and Unit Trusts;

- Land and property in the UK

You can find more information on gifting assets to charity and the tax relief available by visiting the DirectGov website.

Inheritance Tax

Inheritance Tax is paid on an estate when somebody dies. If you leave a gift to charity in your will at least seven years before your death, its value will not be included when valuing your estate (which includes your possessions, property and money) for Inheritance Tax purposes.

Moreover, any estate that is valued at more than the £325,000 Inheritance Tax threshold is eligible for a reduction in Inheritance Tax by donating part of the estate to a registered charity. If you donate 10% or more of the estate to a qualifying UK registered charity, the rate of Inheritance Tax applied to any value in your estate that exceeds the £325,000 threshold will be reduced from 40% to 36% in total tax charged.

However, unfortunately not all parts of the estate may qualify for the reduced rate of Inheritance Tax. It is therefore important to consider whether the 10% donation will benefit your beneficiaries according to the make-up and total value of the entire estate. For more information on reducing your Inheritance Tax bill by donating to charity, visit the HMRC website.

Keeping records of your donations to charity

The importance of record-keeping cannot be understated. In order to reap the benefits of tax relief on charitable giving, it is essential to keep detailed, up-to-date records of all your donations to charity to make sure that you claim the correct amount of tax relief and pay the right amount of tax.

For every tax year, you should keep the following records:

- Details of Gift Aid donations showing the date, the amount and the charities involved;

- Legal documents showing the sale or transfer of assets to charity - including share transfer documents or certificates or land transfer documents;

- Any documentation from a charity asking you to sell land or shares on its behalf

Find out more about keeping records of your gifts to charity

All of the Giving What We Can charities are eligible for Gift Aid if you make a donation via the Giving What We Can trust. Additionally, if you require further information on tax-efficient giving and exactly what you or your chosen charity are eligible for, you can contact the HMRC Charities Helpline.

CAF image source: cafonline.org